Empower Your Compliance Strategy with Blockchain KYC: Unlock Efficiency and Trust

Introduction

In the rapidly evolving digital landscape, the need for efficient and transparent Know Your Customer (KYC) processes is paramount. Traditional KYC methods often face challenges with data accuracy, regulatory compliance, and scalability. Blockchain technology, with its decentralized and immutable nature, offers innovative solutions to streamline KYC processes, reduce operational costs, and enhance trust.

Blockchain KYC: Transforming Compliance

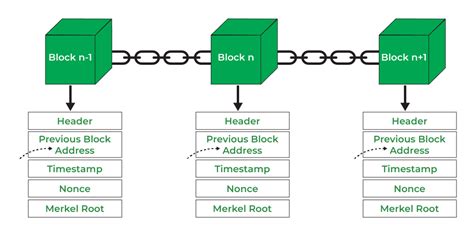

Blockchain KYC leverages the distributed ledger technology to establish a secure and tamper-proof platform for managing customer identity and transaction data. By distributing KYC information across multiple nodes on the network, blockchain eliminates the risk of data forgery and manipulation.

How Blockchain Benefits KYC:

-

Enhanced Data Accuracy: Immutable ledger ensures the integrity and reliability of KYC data.

-

Efficient Validation: Automated smart contracts streamline the verification process, reducing manual errors.

-

Regulatory Compliance: Complies with stringent KYC regulations, such as FATF and AML, ensuring legal adherence.

-

Improved Customer Experience: Simple and user-friendly digital KYC processes enhance customer satisfaction.

-

Cost Reduction: Automates administrative tasks, reducing operating costs significantly.

Inspiring Success Stories

1. Banking Giant's KYC Breakthrough:

A renowned global bank implemented a blockchain-based KYC system, reducing customer onboarding time by 60%. The solution eliminated manual data entry and errors, resulting in significant time and cost savings.

2. Cross-Border KYC Orchestration:

A partnership between fintech firms enabled cross-border KYC for multinational companies. The blockchain platform allowed for secure and compliant data sharing, streamlining the process for businesses operating globally.

3. Government Streamlining KYC:

A government agency adopted blockchain KYC for issuing digital identity documents. The solution provided citizens with safe and verifiable online identities, reducing fraud and improving access to government services.

Understanding the Dynamics

Tables: Breaking Down Key Concepts

| Term |

Definition |

| Know Your Customer (KYC) |

Process of verifying and assessing customer identity and transaction history. |

| Distributed Ledger Technology (DLT) |

Network of computers that maintain a synchronized, tamper-proof record of transactions. |

| Smart Contracts |

Self-executing contracts stored on the blockchain that trigger actions when predefined conditions are met. |

| Blockchain Benefits |

Traditional KYC Challenges |

| Enhanced data security |

Data forgery and manipulation |

| Automated verification |

Manual errors and time-consuming processes |

| Compliance with regulations |

Regulatory compliance issues |

| Improved customer experience |

Complex and lengthy onboarding procedures |

| Cost reduction |

High administrative costs |

Effective Strategies for Blockchain KYC

-

Centralized vs. Decentralized: Consider the appropriate governance model for your organization.

-

Interoperability: Ensure compatibility with existing systems to facilitate seamless data exchange.

-

Data Privacy: Implement robust data protection mechanisms to safeguard customer information.

-

Collaboration: Partner with trusted service providers to enhance KYC capabilities.

-

Regulatory Advocacy: Participate in policy discussions and advocate for the adoption of blockchain KYC standards.

Practical Tips and Tricks

-

Start small: Implement blockchain KYC in specific use cases to gain experience and build confidence.

-

Measure and track results: Regularly monitor the performance and impact of the implemented solution.

-

Educate stakeholders: Communicate the benefits and functionalities of blockchain KYC to foster adoption.

-

Seek expert advice: Consult with knowledgeable professionals or service providers to optimize implementation.

-

Keep up with regulations: Stay informed about evolving KYC regulations to maintain compliance.

Common Mistakes to Avoid

-

Lack of planning: Failing to define clear goals and project requirements can hinder successful implementation.

-

Incompatibility with existing systems: Neglecting the need for integration with legacy systems can create operational challenges.

-

Weak data security: Overlooking the importance of robust data protection measures can compromise customer information.

-

Lack of stakeholder engagement: Failing to involve key stakeholders in the planning and implementation process can lead to resistance and challenges.

-

Inconsistent data management: Failing to establish standardized processes for KYC data collection and management can result in data inaccuracies.

Step-by-Step Approach to Blockchain KYC Implementation

1. Define Goals and Scope: Determine the specific objectives and target areas for blockchain KYC implementation.

2. Build a Team: Assemble a dedicated team with expertise in KYC, blockchain technology, and project management.

3. Select a Blockchain Platform: Evaluate different blockchain platforms based on security, scalability, and regulatory compliance requirements.

4. Develop Smart Contracts: Create smart contracts that define the KYC verification process and automate actions based on predefined conditions.

5. Integrate with Existing Systems: Implement interoperability solutions to connect the blockchain KYC system with legacy systems and data sources.

6. Implement Data Protection Measures: Establish robust security protocols and encryption mechanisms to protect customer information.

7. Conduct User Acceptance Testing: Thoroughly test the solution with real-world scenarios to identify and resolve any potential issues.

8. Launch and Monitor: Deploy the blockchain KYC system and monitor its performance and impact on regulatory compliance and customer experience.

Why Blockchain KYC Matters

Benefits for Businesses:

- Reduced operational costs and improved efficiency.

- Enhanced customer trust and loyalty through transparent and secure KYC processes.

- Compliance with evolving KYC regulations and reduced risk of non-compliance penalties.

Benefits for Customers:

- Simplified and user-friendly onboarding experiences.

- Protection of personal data and reduced risk of identity theft.

- Improved access to financial services and other regulated industries.

Pros and Cons: Balancing Considerations

| Pros |

Cons |

| Decentralized and immutable data |

Limited scalability and performance for complex processes |

| Automated verification and fraud prevention |

Cost and complexity of implementation |

| Improved customer privacy and data security |

Lack of widespread adoption and regulatory frameworks |

| Enhanced trust and transparency |

Potential for cyberattacks and smart contract vulnerabilities |

FAQs: Unraveling Blockchain KYC

1. What are the key challenges in traditional KYC processes?

- Data accuracy, regulatory compliance, scalability, and high operational costs.

2. How does blockchain KYC address these challenges?

- Blockchain's decentralized and immutable nature enhances data integrity, automates verification, streamlines compliance, and reduces costs.

3. What are the potential risks associated with blockchain KYC?

- Cyberattacks, smart contract vulnerabilities, and lack of regulatory clarity.

4. Is blockchain KYC ready for widespread adoption?

- While gaining momentum, blockchain KYC still faces scalability limitations and requires broader regulatory acceptance.

5. How can organizations prepare for the implementation of blockchain KYC?

- Define clear goals, build a skilled team, select a suitable blockchain platform, and implement robust data protection measures.

6. What are the implications of blockchain KYC for customers?

- Simplified onboarding, enhanced privacy, and reduced risk of identity theft.

Call to Action

Embrace the transformative power of blockchain KYC to streamline your compliance processes, enhance trust, and deliver a superior customer experience. Collaborate with trusted service providers, stay informed about evolving regulations, and implement robust data security measures to unlock the full potential of this innovative technology. By adopting blockchain KYC, you not only strengthen your regulatory adherence but also empower your business with increased efficiency, customer satisfaction, and growth opportunities.