Blockchain Technology and KYC: A Comprehensive Guide

Introduction

Blockchain technology is revolutionizing various sectors, and the field of Know Your Customer (KYC) is no exception. KYC plays a crucial role in compliance, fraud prevention, and risk management in financial institutions, and blockchain offers innovative solutions to enhance these processes.

Blockchain for KYC: An Overview

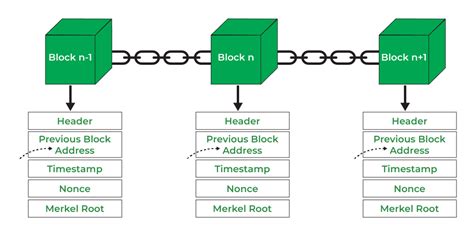

Blockchain is a decentralized, distributed ledger technology that allows for secure and transparent record-keeping. In KYC, blockchain can be utilized to streamline customer onboarding, verify identities, and store compliance data in a tamper-proof manner.

Transitioning to Blockchain-Based KYC

The transition to blockchain-based KYC involves several key steps:

-

Establishing a Governance Framework: Define roles, responsibilities, and policies for managing blockchain-based KYC processes.

-

Selecting a Blockchain Platform: Choose a blockchain platform that aligns with the specific requirements of the organization, such as speed, scalability, and security.

-

Integrating with Existing Systems: Connect the blockchain-based KYC system with existing customer onboarding and data management platforms to ensure seamless integration.

Why Blockchain KYC Matters

Blockchain-based KYC offers numerous benefits compared to traditional systems:

-

Enhanced Security: The distributed nature of blockchain makes it highly resistant to unauthorized access and data tampering.

-

Improved Efficiency: Automating KYC processes through blockchain can significantly reduce onboarding time and costs.

-

Increased Transparency: Blockchain provides a shared, auditable record of all KYC transactions, fostering trust and accountability.

Benefits of Blockchain KYC

Organizations can reap substantial benefits from implementing blockchain-based KYC systems, including:

-

Reduced Fraud Risk: Verified customer identities on the blockchain reduce the likelihood of fraud and financial crime.

-

Improved Regulatory Compliance: Blockchain-based KYC facilitates compliance with regulations such as Anti-Money Laundering (AML) and Counter-Terrorism Financing (CTF).

-

Enhanced Customer Experience: Streamlined KYC processes and reduced onboarding time improve the customer experience.

Strategies for Effective Blockchain KYC

To successfully implement blockchain-based KYC, organizations should consider the following strategies:

-

Collaborate with Industry Leaders: Partner with organizations that have expertise in blockchain and KYC to leverage best practices and technological advancements.

-

Conduct Thorough Due Diligence: Evaluate and select blockchain platforms based on their security, scalability, and regulatory compliance features.

-

Prioritize Data Protection: Ensure that customer data is handled securely and in accordance with privacy regulations.

Step-by-Step Approach to Blockchain KYC

Implementing blockchain-based KYC involves a systematic approach:

-

Define KYC Requirements: Identify the specific KYC requirements and regulatory obligations that need to be addressed.

-

Identify Data Sources: Determine the sources of customer data to be verified on the blockchain, such as government-issued IDs, utility bills, and financial records.

-

Select a Validation Partner: Choose a trusted partner to perform customer identity verification and due diligence checks.

Humorous Stories and Learnings

-

The Case of the Confused Customer: A customer submitted a utility bill as proof of residency during blockchain-based KYC, but the bill was for a water park. Lesson learned: Double-check customer submissions to avoid amusing misunderstandings.

-

The Time Machine KYC: A customer provided a photo of their passport from the 1980s for identity verification. Despite the obvious age discrepancy, the blockchain-based system flagged the passport as valid because the expiration date was still in the future. Lesson learned: Blockchain verifies data as presented, highlighting the importance of accurate customer submissions.

-

The Anonymous KYC: A customer successfully completed blockchain-based KYC using a pseudonym. The organization later realized that the customer was a famous celebrity trying to avoid public exposure. Lesson learned: Pseudonymous transactions on blockchain provide privacy but require additional due diligence to mitigate risks.

Useful Tables

| Comparison of Blockchain KYC Systems |

|---|---|

| Feature | Blockchain-Based KYC | Traditional KYC |

| Security | High (decentralized, immutable) | Moderate (centralized, vulnerable to breaches) |

| Efficiency | High (automated processes) | Low (manual processes) |

| Transparency | Full (shared, auditable record) | Limited (access restricted to specific parties) |

| Benefits of Blockchain KYC for Organizations |

|---|---|

| Benefit | Description |

| Reduced Fraud Risk | Verified identities reduce fraud and financial crime. |

| Improved Regulatory Compliance | Facilitates compliance with AML and CTF regulations. |

| Enhanced Customer Experience | Streamlined KYC processes and reduced onboarding time. |

| Effective Strategies for Blockchain KYC |

|---|---|

| Strategy | Description |

| Collaborate with Industry Leaders | Partner with experts in blockchain and KYC for best practices. |

| Conduct Thorough Due Diligence | Evaluate blockchain platforms based on security, scalability, and compliance. |

| Prioritize Data Protection | Handle customer data securely and in accordance with privacy regulations. |

Call to Action

Embracing blockchain technology for KYC is crucial for organizations seeking to enhance security, efficiency, and compliance. By understanding the benefits, adopting effective strategies, and following a step-by-step approach, organizations can fully leverage the potential of blockchain-based KYC to transform their operations and improve customer experience.